1

/

of

11

www.ChineseStandard.us -- Field Test Asia Pte. Ltd.

GB/T 31277-2022 English PDF (GB/T31277-2022)

GB/T 31277-2022 English PDF (GB/T31277-2022)

Regular price

$290.00

Regular price

Sale price

$290.00

Unit price

/

per

Shipping calculated at checkout.

Couldn't load pickup availability

GB/T 31277-2022: Brand valuation - Retail industry

Delivery: 9 seconds. Download (& Email) true-PDF + Invoice.

Get Quotation: Click GB/T 31277-2022 (Self-service in 1-minute)

Historical versions (Master-website): GB/T 31277-2022

Preview True-PDF (Reload/Scroll-down if blank)

GB/T 31277-2022

NATIONAL STANDARD OF THE

PEOPLE’S REPUBLIC OF CHINA

ICS 03.140

CCS A 00

Replacing GB/T 31277-2014

Brand Valuation – Retail Industry

ISSUED ON: APRIL 15, 2022

IMPLEMENTED ON: NOVEMBER 01, 2022

Issued by: State Administration for Market Regulation;

Standardization Administration of the People’s Republic of China.

Table of Contents

Foreword ... 3

1 Scope ... 5

2 Normative References ... 5

3 Terms and Definitions ... 5

4 Brand Strength ... 5

5 Measurement Model of Brand Value ... 9

6 Evaluation Process of Brand Value ... 11

Appendix A (Informative) Evaluation Indicators and Instructions of Brand Strength 13

Appendix B (Informative) Multi-Cycle Excess Earnings Method ... 16

Appendix C (Informative) Other Optional Evaluation Methods ... 19

Bibliography ... 23

Brand Valuation – Retail Industry

1 Scope

This Document specifies the brand strength, measurement model, and evaluation process for

brand valuation in the retail industry.

This Document is suitable for brand valuation of retail enterprises, and can be used for self-

evaluation or third-party evaluation.

2 Normative References

The provisions in following documents become the essential provisions of this Document

through reference in this Document. For the dated documents, only the versions with the dates

indicated are applicable to this Document; for the undated documents, only the latest version

(including all the amendments) is applicable to this Document.

GB/T 18106 Classification of Retail Formats

GB/T 29185 Brand - Vocabulary

GB/T 29186 (all parts) Evaluation of Brand Value Elements

GB/T 29187 Brand Valuation - Requirements for Monetary Brand Valuation

GB/T 29188 Brand Valuation - Multi-Cycle Excess Earnings Method

3 Terms and Definitions

For the purposes of this Document, the terms and definitions given in GB/T 18106, GB/T 29185,

GB/T 29186 (all parts), GB/T 29187 and GB/T 29188 apply.

4 Brand Strength

4.1 General

The evaluation indicators of brand strength in retail industry include five Level-1 indicators:

tangible elements (K1), quality elements (K2), innovation elements (K3), service elements (K4)

and intangible elements (K5). For the evaluation content, evaluation elements and reference

scores of each Level-1 indicator, see Appendix A.

4.2 Tangible elements

4.2.1 Market performance

Evaluation indicators include but are not limited to:

---market share;

--- coverage.

4.2.2 Finance performance

Evaluation indicators include but are not limited to:

--- profitability;

--- debt paying ability;

--- operating ability;

--- development ability.

4.2.3 Related resources

Evaluation indicators include but are not limited to:

--- the investment of social and human resources;

--- the investment of environmental protection resources.

4.3 Quality elements

4.3.1 Quality management

Evaluation indicators include but are not limited to:

--- construction and operation of quality management system;

--- quality management performance;

--- supply chain management;

--- quality promise.

4.3.2 Commodity quality

4.5.3 Service outcome performance

Evaluation indicators include but are not limited to:

--- service satisfaction;

--- service improvement.

4.6 Intangible elements

4.6.1 Brand culture

Evaluation indicators include but are not limited to:

--- brand strategy;

--- fulfillment of social responsibilities.

4.6.2 Brand management

Evaluation indicators include but are not limited to:

--- management agency;

--- brand investment.

4.6.3 Brand influence

Evaluation indicators include but are not limited to:

--- brand influence;

--- brand honors;

--- brand loyalty;

--- brand history.

4.7 Calculation of brand strength

Brand strength K consists of fiveLevel-1 indicators, namely, tangible elements (K1), quality

elements (K2), innovation elements (K3), service elements (K4) and intangible elements (K5);

and the score is calculated according to Formula (1):

Where:

5.3 Other optional methods

5.3.1 Cost method

5.3.1.1 The cost method is an evaluation method to measure the brand value by deducting the

depreciation caused by various losses and other factors on the basis of the replacement cost of

building the brand. When the cost method is adopted, the evaluated brand shall meet but not

limited to the following conditions:

--- the evaluated brand can continue to be used, that is, it can bring expected benefits to its

owner;

--- have cost information on brand creation and maintenance;

--- be able to measure the depreciation that affects the brand value.

5.3.1.2 For the measurement model of the cost method, refer to the method in C.1 of Appendix

C.

5.3.2 Market method

5.3.2.1 The market method is to measure the value of the evaluated brand by comparing the

similarities and differences of the value of the evaluated brand and the comparable brand, and

adjusting the evaluation value of the comparable brand. When the market method is adopted,

the evaluated brand shall satisfy but not limited to the following conditions:

--- there is a comparable brand similar to the evaluated brand;

--- be able to collect and obtain market information, financial information and other relevant

materials of comparable brands;

--- comparable brands generally select multiple brands in the same industry for comparison,

and select the most reasonable and appropriate brand from them;

--- there is a fully developed and active public market.

NOTE: There are few relevant cases of brands being traded as separate assets. In addition, even if data

on comparable objects are known, the characteristics of the evaluated brands may be significantly

different from those of these few traded brands.

5.3.2.2 For the measurement model of the market method, refer to the method in C.2 of

Appendix C.

5.3.3 Incremental cash flow method

5.3.3.1 The incremental cash flow method identifies the cash flow generated when the company

uses the brand compared with when the brand is not used. When the incremental cash flow

method is adopted, the evaluated brand shall satisfy but not limited to the following conditions:

--- the cash flow that generates cost savings when the subject of evaluation is not using the

brand;

--- the cash flow that generates additional profit when the subject of evaluation is not using

the brand.

5.3.3.2 For the measurement model of the incremental cash flow method, refer to the method

in C.3 of Appendix C.

6 Evaluation Process of Brand Value

6.1 Identify the evaluation purpose

The evaluation purpose is determined based on factors such as the intended use of the

measurement, the user of the result, and the characteristics of the measured brand. Different

evaluation purposes shall affect the evaluation procedure, measurement accuracy and result

reporting form.

6.2 Clarify the factors that influence value

The brand value measured in this Document shall comprehensively consider factors such as

finance, quality, innovation, service, brand building, and market, especially the impact of non-

financial factors such as quality, innovation, service, and market on brand value.

6.3 Describe the measured brand

The brand under evaluation shall be identified, defined and described, including its product

range, value range, etc. before the measurement.

6.4 Determine model parameters

According to the relevant national policies and regulations and the current market economic

situation, determine the evaluation year and evaluation cycle, cash flow forecasting method,

industry average return on assets and other indicators and parameters required for model

measurement.

6.5 Collect measurement data

Following the principles of truthfulness, accuracy and objectivity, collect corporate financial

and other information as input values for corporate or third-party evaluations.

6.6 Execute the measurement process

The measurement process includes:

Appendix B

(Informative)

Multi-Cycle Excess Earnings Method

B.1 Measurement model

The brand value based on the multi-cycle excess earnings method shall be calculated according

to Formula (B.1):

Where:

VB – brand value;

FBC,t – brand earnings in the t year;

FBC,T+1 – brand earnings in the T+1 year;

T - the end year of the forecast period, according to industry and brand characteristics, the

forecast period is generally 3 ~ 5 years;

R – discount rate of brand equity;

g - perpetual growth rate, long-term expected inflation rate can be used.

B.2 Determination of brand earnings

B.2.1 Brand earnings

The brand earnings for the current year, FBC, shall be calculated according to Formula (B.2):

Where:

FBC – brand earnings for the current year;

PA - when the annually-adjusted enterprise income is used, the impact of non-recurring

operating items is considered;

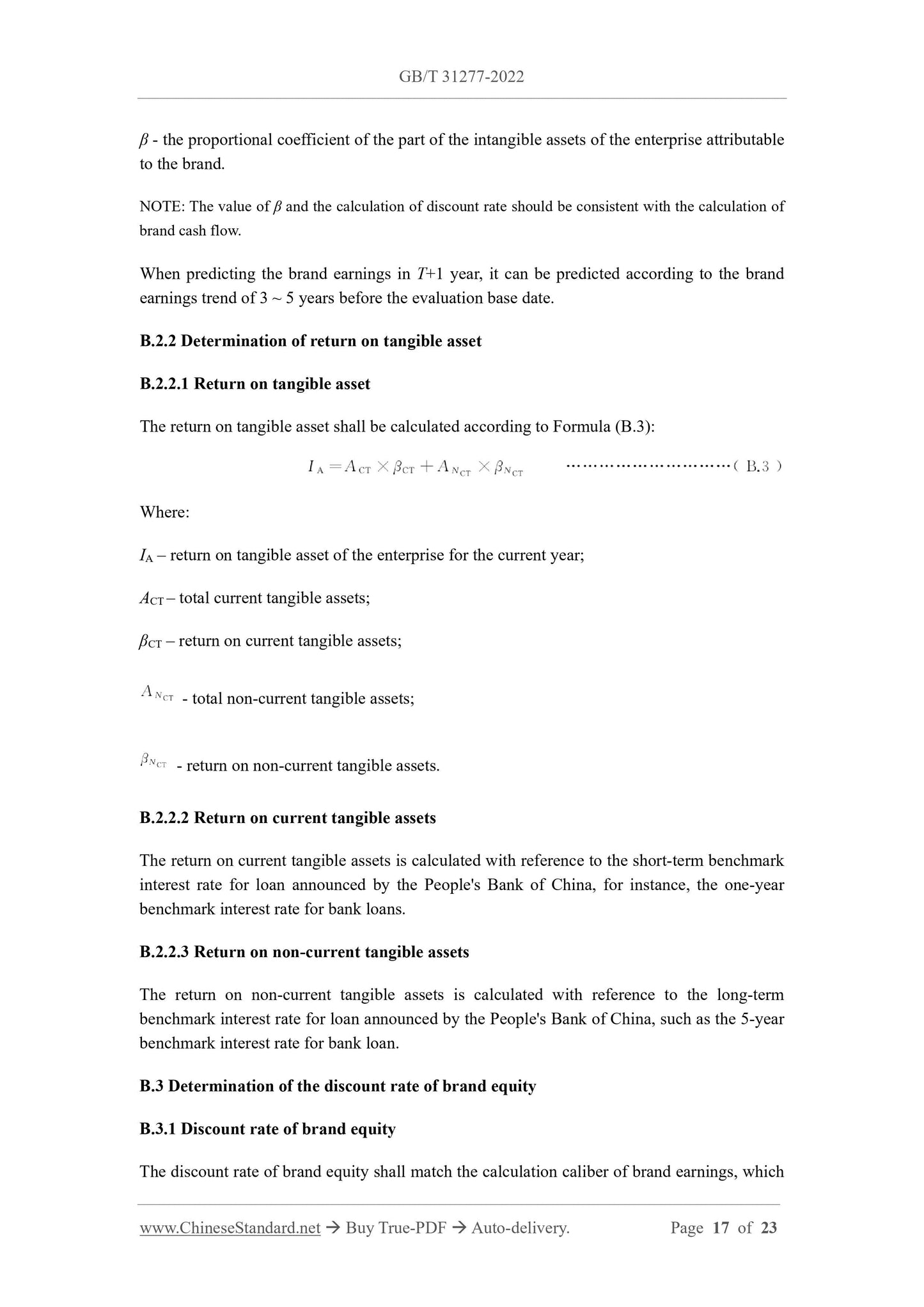

IA - income of tangible assets of the enterprise for the current year;

β - the proportional coefficient of the part of the intangible assets of the enterprise attributable

to the brand.

NOTE: The value of β and the calculation of discount rate should be consistent with the calculation of

brand cash flow.

When predicting the brand earnings in T+1 year, it can be predicted according to the brand

earnings trend of 3 ~ 5 years before the evaluation base date.

B.2.2 Determination of return on tangible asset

B.2.2.1 Return on tangible asset

The return on tangible asset shall be calculated according to Formula (B.3):

Where:

IA – return on tangible asset of the enterprise for the current year;

ACT – total current tangible assets;

βCT – return on current tangible assets;

- total non-current tangible assets;

- return on non-current tangible assets.

B.2.2.2 Return on current tangible assets

The return on current tangible assets is calculated with reference to the short-term benchmark

interest rate for loan announced by the People's Bank of China, for instance, the one-year

benchmark interest rate for bank loans.

B.2.2.3 Return on non-current tangible assets

The return on non-current tangible assets is calculated with reference to the long-term

benchmark interest rate for loan announced by the People's Bank of China, such as the 5-year

benchmark interest rate for bank loan.

B.3 Determination of the discount rate of brand equity

B.3.1 Discount rate of brand equity

The discount rate of brand equity shall match the calculation caliber of brand earnings, which

Appendix C

(Informative)

Other Optional Evaluation Methods

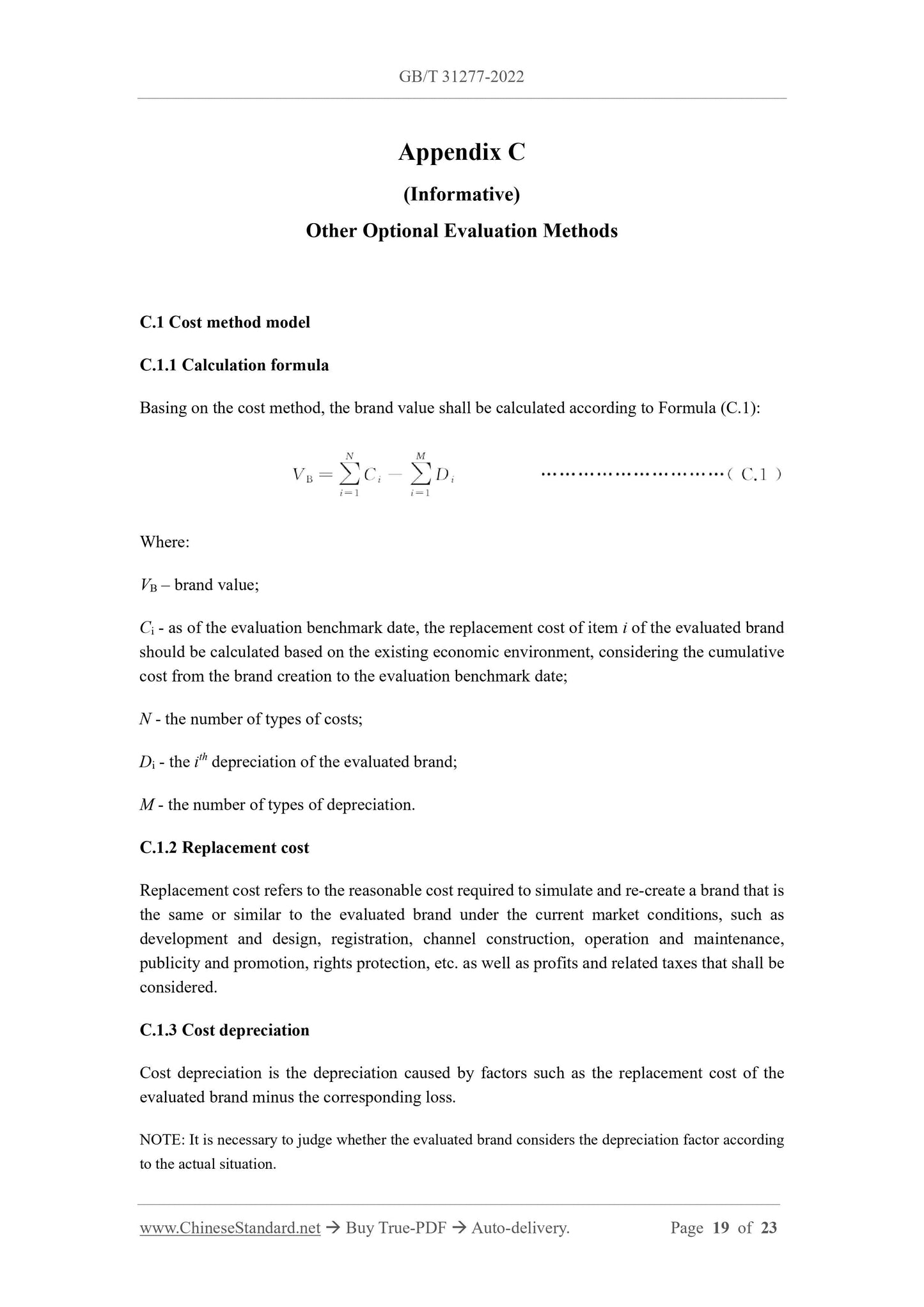

C.1 Cost method model

C.1.1 Calculation formula

Basing on the cost method, the brand value shall be calculated according to Formula (C.1):

Where:

VB – brand value;

Ci - as of the evaluation benchmark date, the replacement cost of item i of the evaluated brand

should be calculated based on the existing economic environment, considering the cumulative

cost from the brand creation to the evaluation benchmark date;

N - the number of types of costs;

Di - the ith depreciation of the evaluated brand;

M - the number of types of depreciation.

C.1.2 Replacement cost

Replacement cost refers to the reasonable cost required to simulate and re-create a brand that is

the same or similar to the evaluated brand under the current market conditions, such as

development and design, registration, channel construction, operation and maintenance,

publicity and promotion, rights protection, etc. as well as profits and related taxes that shall be

considered.

C.1.3 Cost depreciation

Cost depreciation is the depreciation caused by factors such as the replacement cost of the

evaluated brand minus the corresponding loss.

NOTE: It is necessary to judge whether the evaluated brand considers the depreciation factor according

to the actual situation.

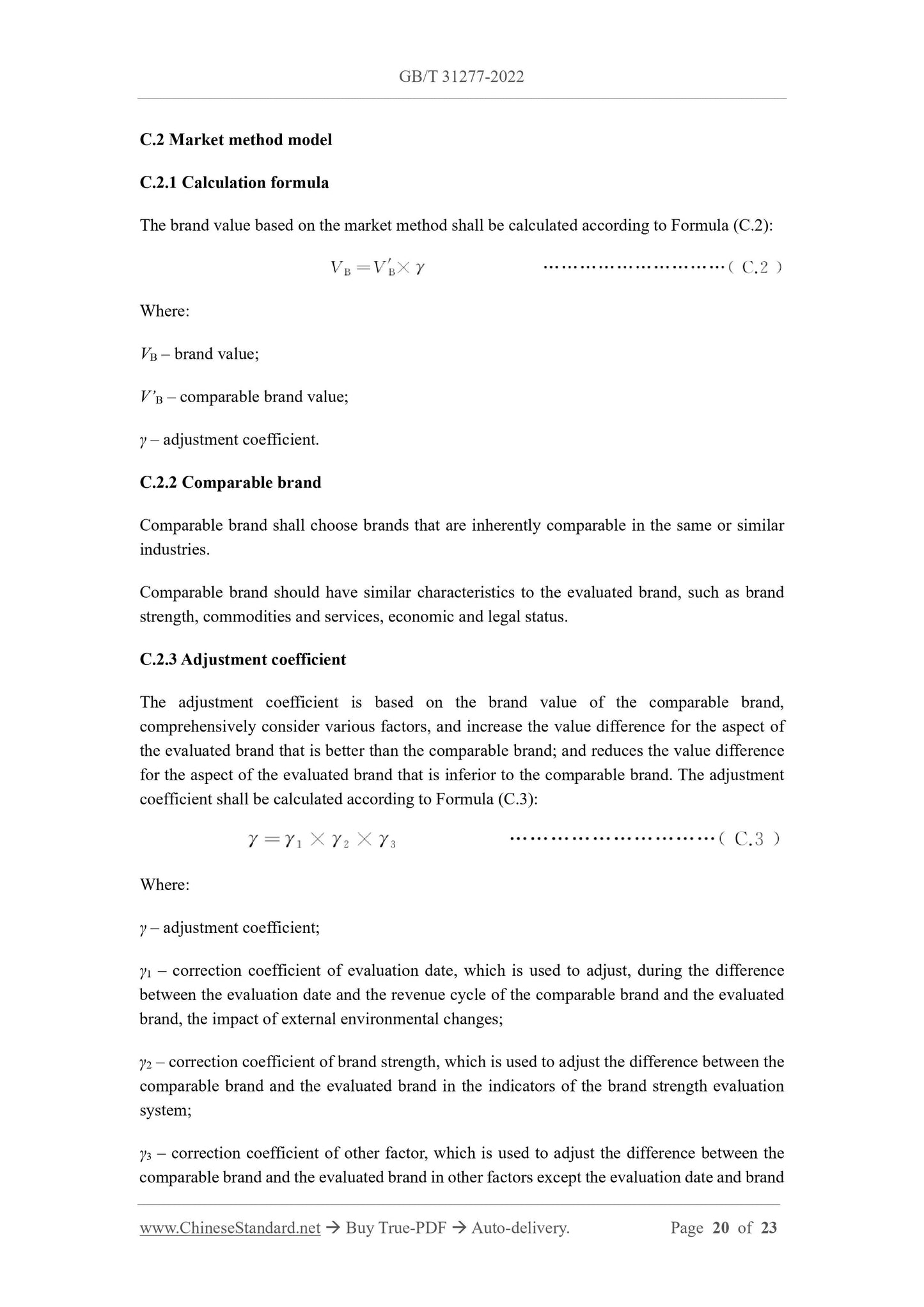

C.2 Market method model

C.2.1 Calculation formula

The brand value based on the market method shall be calculated according to Formula (C.2):

Where:

VB – brand value;

V’B – comparable brand value;

γ – adjustment coefficient.

C.2.2 Comparable brand

Comparable brand shall choose brands that are inherently comparable in the same or similar

industries.

Comparable brand should have similar characteristics to the evaluated brand, such as brand

strength, commodities and services, economic and legal status.

C.2.3 Adjustment coefficient

The adjustment coefficient is based on the brand value of the comparable brand,

comprehensively consider various factors, and increase the value difference for the aspect of

the evaluated brand that is better than the comparable brand; and reduces the value difference

for the aspect of the evaluated brand that is inferior to the comparable brand. The adjustment

coefficient shall be calculated according to Formula (C.3):

Where:

γ – adjustment coefficient;

γ1 – correction coefficient of evaluation date, which is used to adjust, during the difference

between the evaluation date and the revenue cycle of the comparable brand and the evaluated

brand, the impact of external environmental changes;

γ2 – correction coefficient of brand strength, which is used to adjust the difference between the

comparable brand and the evaluated brand in the indicators of the brand strength evaluation

system;

γ3 – correction coefficient of other factor, which is used to adjust the difference between the

comparable brand and the evaluated brand in other factors except the evaluation date and brand

GB/T 31277-2022

NATIONAL STANDARD OF THE

PEOPLE’S REPUBLIC OF CHINA

ICS 03.140

CCS A 00

Replacing GB/T 31277-2014

Brand Valuation – Retail Industry

ISSUED ON: APRIL 15, 2022

IMPLEMENTED ON: NOVEMBER 01, 2022

Issued by: State Administration for Market Regulation;

Standardization Administration of the People’s Republic of China.

Table of Contents

Foreword ... 3

1 Scope ... 5

2 Normative References ... 5

3 Terms and Definitions ... 5

4 Brand Strength ... 5

5 Measurement Model of Brand Value ... 9

6 Evaluation...

Delivery: 9 seconds. Download (& Email) true-PDF + Invoice.

Get Quotation: Click GB/T 31277-2022 (Self-service in 1-minute)

Historical versions (Master-website): GB/T 31277-2022

Preview True-PDF (Reload/Scroll-down if blank)

GB/T 31277-2022

NATIONAL STANDARD OF THE

PEOPLE’S REPUBLIC OF CHINA

ICS 03.140

CCS A 00

Replacing GB/T 31277-2014

Brand Valuation – Retail Industry

ISSUED ON: APRIL 15, 2022

IMPLEMENTED ON: NOVEMBER 01, 2022

Issued by: State Administration for Market Regulation;

Standardization Administration of the People’s Republic of China.

Table of Contents

Foreword ... 3

1 Scope ... 5

2 Normative References ... 5

3 Terms and Definitions ... 5

4 Brand Strength ... 5

5 Measurement Model of Brand Value ... 9

6 Evaluation Process of Brand Value ... 11

Appendix A (Informative) Evaluation Indicators and Instructions of Brand Strength 13

Appendix B (Informative) Multi-Cycle Excess Earnings Method ... 16

Appendix C (Informative) Other Optional Evaluation Methods ... 19

Bibliography ... 23

Brand Valuation – Retail Industry

1 Scope

This Document specifies the brand strength, measurement model, and evaluation process for

brand valuation in the retail industry.

This Document is suitable for brand valuation of retail enterprises, and can be used for self-

evaluation or third-party evaluation.

2 Normative References

The provisions in following documents become the essential provisions of this Document

through reference in this Document. For the dated documents, only the versions with the dates

indicated are applicable to this Document; for the undated documents, only the latest version

(including all the amendments) is applicable to this Document.

GB/T 18106 Classification of Retail Formats

GB/T 29185 Brand - Vocabulary

GB/T 29186 (all parts) Evaluation of Brand Value Elements

GB/T 29187 Brand Valuation - Requirements for Monetary Brand Valuation

GB/T 29188 Brand Valuation - Multi-Cycle Excess Earnings Method

3 Terms and Definitions

For the purposes of this Document, the terms and definitions given in GB/T 18106, GB/T 29185,

GB/T 29186 (all parts), GB/T 29187 and GB/T 29188 apply.

4 Brand Strength

4.1 General

The evaluation indicators of brand strength in retail industry include five Level-1 indicators:

tangible elements (K1), quality elements (K2), innovation elements (K3), service elements (K4)

and intangible elements (K5). For the evaluation content, evaluation elements and reference

scores of each Level-1 indicator, see Appendix A.

4.2 Tangible elements

4.2.1 Market performance

Evaluation indicators include but are not limited to:

---market share;

--- coverage.

4.2.2 Finance performance

Evaluation indicators include but are not limited to:

--- profitability;

--- debt paying ability;

--- operating ability;

--- development ability.

4.2.3 Related resources

Evaluation indicators include but are not limited to:

--- the investment of social and human resources;

--- the investment of environmental protection resources.

4.3 Quality elements

4.3.1 Quality management

Evaluation indicators include but are not limited to:

--- construction and operation of quality management system;

--- quality management performance;

--- supply chain management;

--- quality promise.

4.3.2 Commodity quality

4.5.3 Service outcome performance

Evaluation indicators include but are not limited to:

--- service satisfaction;

--- service improvement.

4.6 Intangible elements

4.6.1 Brand culture

Evaluation indicators include but are not limited to:

--- brand strategy;

--- fulfillment of social responsibilities.

4.6.2 Brand management

Evaluation indicators include but are not limited to:

--- management agency;

--- brand investment.

4.6.3 Brand influence

Evaluation indicators include but are not limited to:

--- brand influence;

--- brand honors;

--- brand loyalty;

--- brand history.

4.7 Calculation of brand strength

Brand strength K consists of fiveLevel-1 indicators, namely, tangible elements (K1), quality

elements (K2), innovation elements (K3), service elements (K4) and intangible elements (K5);

and the score is calculated according to Formula (1):

Where:

5.3 Other optional methods

5.3.1 Cost method

5.3.1.1 The cost method is an evaluation method to measure the brand value by deducting the

depreciation caused by various losses and other factors on the basis of the replacement cost of

building the brand. When the cost method is adopted, the evaluated brand shall meet but not

limited to the following conditions:

--- the evaluated brand can continue to be used, that is, it can bring expected benefits to its

owner;

--- have cost information on brand creation and maintenance;

--- be able to measure the depreciation that affects the brand value.

5.3.1.2 For the measurement model of the cost method, refer to the method in C.1 of Appendix

C.

5.3.2 Market method

5.3.2.1 The market method is to measure the value of the evaluated brand by comparing the

similarities and differences of the value of the evaluated brand and the comparable brand, and

adjusting the evaluation value of the comparable brand. When the market method is adopted,

the evaluated brand shall satisfy but not limited to the following conditions:

--- there is a comparable brand similar to the evaluated brand;

--- be able to collect and obtain market information, financial information and other relevant

materials of comparable brands;

--- comparable brands generally select multiple brands in the same industry for comparison,

and select the most reasonable and appropriate brand from them;

--- there is a fully developed and active public market.

NOTE: There are few relevant cases of brands being traded as separate assets. In addition, even if data

on comparable objects are known, the characteristics of the evaluated brands may be significantly

different from those of these few traded brands.

5.3.2.2 For the measurement model of the market method, refer to the method in C.2 of

Appendix C.

5.3.3 Incremental cash flow method

5.3.3.1 The incremental cash flow method identifies the cash flow generated when the company

uses the brand compared with when the brand is not used. When the incremental cash flow

method is adopted, the evaluated brand shall satisfy but not limited to the following conditions:

--- the cash flow that generates cost savings when the subject of evaluation is not using the

brand;

--- the cash flow that generates additional profit when the subject of evaluation is not using

the brand.

5.3.3.2 For the measurement model of the incremental cash flow method, refer to the method

in C.3 of Appendix C.

6 Evaluation Process of Brand Value

6.1 Identify the evaluation purpose

The evaluation purpose is determined based on factors such as the intended use of the

measurement, the user of the result, and the characteristics of the measured brand. Different

evaluation purposes shall affect the evaluation procedure, measurement accuracy and result

reporting form.

6.2 Clarify the factors that influence value

The brand value measured in this Document shall comprehensively consider factors such as

finance, quality, innovation, service, brand building, and market, especially the impact of non-

financial factors such as quality, innovation, service, and market on brand value.

6.3 Describe the measured brand

The brand under evaluation shall be identified, defined and described, including its product

range, value range, etc. before the measurement.

6.4 Determine model parameters

According to the relevant national policies and regulations and the current market economic

situation, determine the evaluation year and evaluation cycle, cash flow forecasting method,

industry average return on assets and other indicators and parameters required for model

measurement.

6.5 Collect measurement data

Following the principles of truthfulness, accuracy and objectivity, collect corporate financial

and other information as input values for corporate or third-party evaluations.

6.6 Execute the measurement process

The measurement process includes:

Appendix B

(Informative)

Multi-Cycle Excess Earnings Method

B.1 Measurement model

The brand value based on the multi-cycle excess earnings method shall be calculated according

to Formula (B.1):

Where:

VB – brand value;

FBC,t – brand earnings in the t year;

FBC,T+1 – brand earnings in the T+1 year;

T - the end year of the forecast period, according to industry and brand characteristics, the

forecast period is generally 3 ~ 5 years;

R – discount rate of brand equity;

g - perpetual growth rate, long-term expected inflation rate can be used.

B.2 Determination of brand earnings

B.2.1 Brand earnings

The brand earnings for the current year, FBC, shall be calculated according to Formula (B.2):

Where:

FBC – brand earnings for the current year;

PA - when the annually-adjusted enterprise income is used, the impact of non-recurring

operating items is considered;

IA - income of tangible assets of the enterprise for the current year;

β - the proportional coefficient of the part of the intangible assets of the enterprise attributable

to the brand.

NOTE: The value of β and the calculation of discount rate should be consistent with the calculation of

brand cash flow.

When predicting the brand earnings in T+1 year, it can be predicted according to the brand

earnings trend of 3 ~ 5 years before the evaluation base date.

B.2.2 Determination of return on tangible asset

B.2.2.1 Return on tangible asset

The return on tangible asset shall be calculated according to Formula (B.3):

Where:

IA – return on tangible asset of the enterprise for the current year;

ACT – total current tangible assets;

βCT – return on current tangible assets;

- total non-current tangible assets;

- return on non-current tangible assets.

B.2.2.2 Return on current tangible assets

The return on current tangible assets is calculated with reference to the short-term benchmark

interest rate for loan announced by the People's Bank of China, for instance, the one-year

benchmark interest rate for bank loans.

B.2.2.3 Return on non-current tangible assets

The return on non-current tangible assets is calculated with reference to the long-term

benchmark interest rate for loan announced by the People's Bank of China, such as the 5-year

benchmark interest rate for bank loan.

B.3 Determination of the discount rate of brand equity

B.3.1 Discount rate of brand equity

The discount rate of brand equity shall match the calculation caliber of brand earnings, which

Appendix C

(Informative)

Other Optional Evaluation Methods

C.1 Cost method model

C.1.1 Calculation formula

Basing on the cost method, the brand value shall be calculated according to Formula (C.1):

Where:

VB – brand value;

Ci - as of the evaluation benchmark date, the replacement cost of item i of the evaluated brand

should be calculated based on the existing economic environment, considering the cumulative

cost from the brand creation to the evaluation benchmark date;

N - the number of types of costs;

Di - the ith depreciation of the evaluated brand;

M - the number of types of depreciation.

C.1.2 Replacement cost

Replacement cost refers to the reasonable cost required to simulate and re-create a brand that is

the same or similar to the evaluated brand under the current market conditions, such as

development and design, registration, channel construction, operation and maintenance,

publicity and promotion, rights protection, etc. as well as profits and related taxes that shall be

considered.

C.1.3 Cost depreciation

Cost depreciation is the depreciation caused by factors such as the replacement cost of the

evaluated brand minus the corresponding loss.

NOTE: It is necessary to judge whether the evaluated brand considers the depreciation factor according

to the actual situation.

C.2 Market method model

C.2.1 Calculation formula

The brand value based on the market method shall be calculated according to Formula (C.2):

Where:

VB – brand value;

V’B – comparable brand value;

γ – adjustment coefficient.

C.2.2 Comparable brand

Comparable brand shall choose brands that are inherently comparable in the same or similar

industries.

Comparable brand should have similar characteristics to the evaluated brand, such as brand

strength, commodities and services, economic and legal status.

C.2.3 Adjustment coefficient

The adjustment coefficient is based on the brand value of the comparable brand,

comprehensively consider various factors, and increase the value difference for the aspect of

the evaluated brand that is better than the comparable brand; and reduces the value difference

for the aspect of the evaluated brand that is inferior to the comparable brand. The adjustment

coefficient shall be calculated according to Formula (C.3):

Where:

γ – adjustment coefficient;

γ1 – correction coefficient of evaluation date, which is used to adjust, during the difference

between the evaluation date and the revenue cycle of the comparable brand and the evaluated

brand, the impact of external environmental changes;

γ2 – correction coefficient of brand strength, which is used to adjust the difference between the

comparable brand and the evaluated brand in the indicators of the brand strength evaluation

system;

γ3 – correction coefficient of other factor, which is used to adjust the difference between the

comparable brand and the evaluated brand in other factors except the evaluation date and brand

GB/T 31277-2022

NATIONAL STANDARD OF THE

PEOPLE’S REPUBLIC OF CHINA

ICS 03.140

CCS A 00

Replacing GB/T 31277-2014

Brand Valuation – Retail Industry

ISSUED ON: APRIL 15, 2022

IMPLEMENTED ON: NOVEMBER 01, 2022

Issued by: State Administration for Market Regulation;

Standardization Administration of the People’s Republic of China.

Table of Contents

Foreword ... 3

1 Scope ... 5

2 Normative References ... 5

3 Terms and Definitions ... 5

4 Brand Strength ... 5

5 Measurement Model of Brand Value ... 9

6 Evaluation...

Share